User login

Child of The New Gastroenterologist

Gastroenterology billing and coding: Just the basics

Understanding the business side of medicine helps physicians run a successful practice. However, the business side of medicine is not part of the normal curriculum in training and fellowship programs. Physicians come out of training with the knowledge to treat patients but with little or no knowledge of how to get reimbursed for their services. Gastroenterologists provide both medical and surgical services.

Listed below are some of the basic principles for both documentation and reimbursement policies. All reimbursement is based upon Relative Value Units (RVUs) assigned to every service provided. The services are based upon three factors: physician work value, malpractice cost, and practice expense. Those factors added together and multiplied by a conversion factor assigned by the Centers for Medicare & Medicaid Services (CMS) creates the national physician fee schedule. Each Medicare carrier has localities, and there is another percentage that is multiplied based upon geographic location, which will finalize the approved amount for each service. Your Medicare carrier has the actual approved amounts available on their websites with an effective date of Jan. 1. Commercial payers most commonly base contracts on the Medicare Fee Schedule, but each practice and payer relationship is different. For a better understanding, please contact your practice manager for more specific information based on your payer contracts.

Medical necessity is the key to success. If medical necessity is not demonstrated, payers can deny a claim, deny authorization for a lab test and/or diagnostic study, or recoup previously paid claims. Medicare and commercial payers will often have local coverage determinations (LCDs) for procedures and testing that include indications and restrictions along with approved diagnosis codes. Listed below are the four primary services that GI providers perform and provide interpretation for:

1. Evaluation and management (E&M) services: There are three criteria that have to be met to support any initial visit with patients: the history obtained, the examination performed, and the development of the treatment plan. There are five levels of service for office visits and three levels for inpatient visits, respectively. The levels are chosen based on the decision-making element of the visit, provided the documentation requirements are met for the level chosen. This is often not an easy selection unless the providers are educated on the E&M criteria. Auditors often see that visits are chosen by “guessing” the level, which leads to choosing either a lower or higher level of service than what was actually provided. Some providers have been instructed that E&M services are not that important since procedures are the major source of revenue for the practice. However, GI practices are visit-driven practices, and the initial visits are often worth more RVUs than some procedures. The E&M visit is truly vital and often the backbone for the medical necessity of any additional procedures and diagnostic services required in order for successful treatment of the patient.

2. Endoscopy and procedural billing: Here, medical necessity must be documented in order to submit charges for what was done. Gastroenterologists will often use multiple techniques when treating different areas within the gastrointestinal tract. Documentation has to include the location of lesions/abnormalities, method of treatment/removal, and the reason(s)/indication(s) for those procedures. There may be different instruments used in the colon (for example, snare in the sigmoid colon or biopsy forceps in the transverse colon). These may be separately reported with an appropriate modifier to indicate that these services were performed to different lesions/abnormalities. However, in order to bill for each of the procedures, all of this has to be documented in the endoscopy report. The physician is responsible for accurate and specific documentation and bringing charges back to the billing staff for claim submission. For a successful practice, a team approach is vital. Physicians and coding staff need to have an open line of communication to make sure that everything is submitted appropriately according to payer policies. Billing staff need to communicate any significant changes to the physicians/providers as these changes occur. Ignorance of payer policy is not considered an appropriate excuse when a payer investigates a claim and potential recoupment of moneys paid.

3. Diagnostic studies: Medical necessity/indication for the testing must be documented in order to submit charges for diagnostic studies. The terms “rule out” and “suspect” don’t completely give coders the reason why a physician suspects the patient might have a condition. Usually, abnormal lab tests, signs, and symptoms will often warrant the need for further investigation, and these are the most crucial indications for testing. Not only is this important for diagnostic studies but also for procedures. Make sure that the interpretation of the test results is clear along with a plan/recommendation(s).

4. Diagnosis codes: Assignment of codes per the International Classification of Diseases, 10th revision, Clinical Modification (ICD-10-CM) is the next and most important step after a visit, diagnostic study, and/or procedure. These codes support medical necessity for the services provided, and specificity of the diagnosis code is vital to successful submission and payment of a claim. Signs and symptoms are valid code choices when ruling out a more significant disease/diagnosis because these support medical necessity for a work-up to determine etiology. Comorbidities that impact the provider’s decision making should also be added as additional diagnoses to support the higher level of decision making. Up to 12 diagnosis codes can be assigned to any type of service provided. This also applies to preauthorization of all services, such as lab tests, radiology studies, GI diagnostic studies, and procedures. If specific information is not in the documentation for your staff to access, payers will often deny certain lab and radiology studies, as well as some procedures. There are 71,932 ICD-10-CM codes to choose from, and it is often difficult to find the “specific” code when doing a search in the electronic health record and billing system. Education and training are essential during the orientation sessions prior to active employment, as well as any time the system is upgraded. The providers should be willing to work with the IT representative(s) in the practice to help make the information easier to access. In other words, what “buzz” words would they like included in the description of the ICD-10-CM code in the practice’s list of favorites? For example, Crohn’s disease and ulcerative colitis have over a hundred choices. The choices are based on the location of the disease and whether the disease is without or with complications. If you are going to choose to provide a higher level of E&M service for a patient with Crohn’s disease of the large intestine because of exacerbation of the disease with bleeding, then the appropriate diagnosis code would be one of the following:

- K50.10 Crohn’s disease of large intestine without complications.

- K50.111 Crohn’s disease of large intestine with rectal bleeding.

- K50.112 Crohn’s disease of large intestine with intestinal obstruction.

- K50.113 Crohn’s disease of large intestine with fistula.

- K50.114 Crohn’s disease of large intestine with abscess.

- K50.118 Crohn’s disease of large intestine with other complication.

- K50.119 Crohn’s disease of large intestine with unspecified complications.

Getting paid for your provided services requires attention to detail and communication with your entire staffing team, including all providers. Make sure that your team is educated on all current issues and services pertaining to gastroenterology practices. If there is ever a question when reviewing a procedure note or any service, ask the provider who performed that service. Often, there will have to be legal corrections to the note before services can be billed. Making sure that the claim you are submitting is “clean” is essential for prompt payment. There are multiple resources available through the AGA that will help guide you with coding and billing. There are webinars, training sessions, and onsite services available via http://agau.gastro.org/diweb/catalog that can be provided for all providers, coding and billing staff, administrators, and clinical staff. Everyone needs to take an active role.

Ms. Mueller is a health care consultant with more than 35 years of experience in health care, including ICU/CCU nursing, physician office administration, GI claims submission and adjudication, and seminar instruction. She is president and owner of AskMueller Consulting in Lenzburg, Ill., which provides consulting services for physicians nationwide. Ms. Mueller is a nationally known speaker and the author of many multispecialty medical and surgical coding workbooks. She has a great amount of experience in gastroenterology, surgical subspecialties, and pediatric subspecialties. Her presentations have had audiences with the American Gastroenterological Association (AGA), North American Society for Pediatric Gastroenterology and Nutrition (NASPGAN), Society of Gastroenterology Nurses and Associates, Digestive Disease Week, American Pediatric Surgical Associations, and Decision Health and the Coding Institute. Ms. Mueller has written coding columns for ASGE, NASPGHAN, and AGA. She is the coeditor of the ASGE Coding Primer and also answers the coding hotline for the ASGE.

Understanding the business side of medicine helps physicians run a successful practice. However, the business side of medicine is not part of the normal curriculum in training and fellowship programs. Physicians come out of training with the knowledge to treat patients but with little or no knowledge of how to get reimbursed for their services. Gastroenterologists provide both medical and surgical services.

Listed below are some of the basic principles for both documentation and reimbursement policies. All reimbursement is based upon Relative Value Units (RVUs) assigned to every service provided. The services are based upon three factors: physician work value, malpractice cost, and practice expense. Those factors added together and multiplied by a conversion factor assigned by the Centers for Medicare & Medicaid Services (CMS) creates the national physician fee schedule. Each Medicare carrier has localities, and there is another percentage that is multiplied based upon geographic location, which will finalize the approved amount for each service. Your Medicare carrier has the actual approved amounts available on their websites with an effective date of Jan. 1. Commercial payers most commonly base contracts on the Medicare Fee Schedule, but each practice and payer relationship is different. For a better understanding, please contact your practice manager for more specific information based on your payer contracts.

Medical necessity is the key to success. If medical necessity is not demonstrated, payers can deny a claim, deny authorization for a lab test and/or diagnostic study, or recoup previously paid claims. Medicare and commercial payers will often have local coverage determinations (LCDs) for procedures and testing that include indications and restrictions along with approved diagnosis codes. Listed below are the four primary services that GI providers perform and provide interpretation for:

1. Evaluation and management (E&M) services: There are three criteria that have to be met to support any initial visit with patients: the history obtained, the examination performed, and the development of the treatment plan. There are five levels of service for office visits and three levels for inpatient visits, respectively. The levels are chosen based on the decision-making element of the visit, provided the documentation requirements are met for the level chosen. This is often not an easy selection unless the providers are educated on the E&M criteria. Auditors often see that visits are chosen by “guessing” the level, which leads to choosing either a lower or higher level of service than what was actually provided. Some providers have been instructed that E&M services are not that important since procedures are the major source of revenue for the practice. However, GI practices are visit-driven practices, and the initial visits are often worth more RVUs than some procedures. The E&M visit is truly vital and often the backbone for the medical necessity of any additional procedures and diagnostic services required in order for successful treatment of the patient.

2. Endoscopy and procedural billing: Here, medical necessity must be documented in order to submit charges for what was done. Gastroenterologists will often use multiple techniques when treating different areas within the gastrointestinal tract. Documentation has to include the location of lesions/abnormalities, method of treatment/removal, and the reason(s)/indication(s) for those procedures. There may be different instruments used in the colon (for example, snare in the sigmoid colon or biopsy forceps in the transverse colon). These may be separately reported with an appropriate modifier to indicate that these services were performed to different lesions/abnormalities. However, in order to bill for each of the procedures, all of this has to be documented in the endoscopy report. The physician is responsible for accurate and specific documentation and bringing charges back to the billing staff for claim submission. For a successful practice, a team approach is vital. Physicians and coding staff need to have an open line of communication to make sure that everything is submitted appropriately according to payer policies. Billing staff need to communicate any significant changes to the physicians/providers as these changes occur. Ignorance of payer policy is not considered an appropriate excuse when a payer investigates a claim and potential recoupment of moneys paid.

3. Diagnostic studies: Medical necessity/indication for the testing must be documented in order to submit charges for diagnostic studies. The terms “rule out” and “suspect” don’t completely give coders the reason why a physician suspects the patient might have a condition. Usually, abnormal lab tests, signs, and symptoms will often warrant the need for further investigation, and these are the most crucial indications for testing. Not only is this important for diagnostic studies but also for procedures. Make sure that the interpretation of the test results is clear along with a plan/recommendation(s).

4. Diagnosis codes: Assignment of codes per the International Classification of Diseases, 10th revision, Clinical Modification (ICD-10-CM) is the next and most important step after a visit, diagnostic study, and/or procedure. These codes support medical necessity for the services provided, and specificity of the diagnosis code is vital to successful submission and payment of a claim. Signs and symptoms are valid code choices when ruling out a more significant disease/diagnosis because these support medical necessity for a work-up to determine etiology. Comorbidities that impact the provider’s decision making should also be added as additional diagnoses to support the higher level of decision making. Up to 12 diagnosis codes can be assigned to any type of service provided. This also applies to preauthorization of all services, such as lab tests, radiology studies, GI diagnostic studies, and procedures. If specific information is not in the documentation for your staff to access, payers will often deny certain lab and radiology studies, as well as some procedures. There are 71,932 ICD-10-CM codes to choose from, and it is often difficult to find the “specific” code when doing a search in the electronic health record and billing system. Education and training are essential during the orientation sessions prior to active employment, as well as any time the system is upgraded. The providers should be willing to work with the IT representative(s) in the practice to help make the information easier to access. In other words, what “buzz” words would they like included in the description of the ICD-10-CM code in the practice’s list of favorites? For example, Crohn’s disease and ulcerative colitis have over a hundred choices. The choices are based on the location of the disease and whether the disease is without or with complications. If you are going to choose to provide a higher level of E&M service for a patient with Crohn’s disease of the large intestine because of exacerbation of the disease with bleeding, then the appropriate diagnosis code would be one of the following:

- K50.10 Crohn’s disease of large intestine without complications.

- K50.111 Crohn’s disease of large intestine with rectal bleeding.

- K50.112 Crohn’s disease of large intestine with intestinal obstruction.

- K50.113 Crohn’s disease of large intestine with fistula.

- K50.114 Crohn’s disease of large intestine with abscess.

- K50.118 Crohn’s disease of large intestine with other complication.

- K50.119 Crohn’s disease of large intestine with unspecified complications.

Getting paid for your provided services requires attention to detail and communication with your entire staffing team, including all providers. Make sure that your team is educated on all current issues and services pertaining to gastroenterology practices. If there is ever a question when reviewing a procedure note or any service, ask the provider who performed that service. Often, there will have to be legal corrections to the note before services can be billed. Making sure that the claim you are submitting is “clean” is essential for prompt payment. There are multiple resources available through the AGA that will help guide you with coding and billing. There are webinars, training sessions, and onsite services available via http://agau.gastro.org/diweb/catalog that can be provided for all providers, coding and billing staff, administrators, and clinical staff. Everyone needs to take an active role.

Ms. Mueller is a health care consultant with more than 35 years of experience in health care, including ICU/CCU nursing, physician office administration, GI claims submission and adjudication, and seminar instruction. She is president and owner of AskMueller Consulting in Lenzburg, Ill., which provides consulting services for physicians nationwide. Ms. Mueller is a nationally known speaker and the author of many multispecialty medical and surgical coding workbooks. She has a great amount of experience in gastroenterology, surgical subspecialties, and pediatric subspecialties. Her presentations have had audiences with the American Gastroenterological Association (AGA), North American Society for Pediatric Gastroenterology and Nutrition (NASPGAN), Society of Gastroenterology Nurses and Associates, Digestive Disease Week, American Pediatric Surgical Associations, and Decision Health and the Coding Institute. Ms. Mueller has written coding columns for ASGE, NASPGHAN, and AGA. She is the coeditor of the ASGE Coding Primer and also answers the coding hotline for the ASGE.

Understanding the business side of medicine helps physicians run a successful practice. However, the business side of medicine is not part of the normal curriculum in training and fellowship programs. Physicians come out of training with the knowledge to treat patients but with little or no knowledge of how to get reimbursed for their services. Gastroenterologists provide both medical and surgical services.

Listed below are some of the basic principles for both documentation and reimbursement policies. All reimbursement is based upon Relative Value Units (RVUs) assigned to every service provided. The services are based upon three factors: physician work value, malpractice cost, and practice expense. Those factors added together and multiplied by a conversion factor assigned by the Centers for Medicare & Medicaid Services (CMS) creates the national physician fee schedule. Each Medicare carrier has localities, and there is another percentage that is multiplied based upon geographic location, which will finalize the approved amount for each service. Your Medicare carrier has the actual approved amounts available on their websites with an effective date of Jan. 1. Commercial payers most commonly base contracts on the Medicare Fee Schedule, but each practice and payer relationship is different. For a better understanding, please contact your practice manager for more specific information based on your payer contracts.

Medical necessity is the key to success. If medical necessity is not demonstrated, payers can deny a claim, deny authorization for a lab test and/or diagnostic study, or recoup previously paid claims. Medicare and commercial payers will often have local coverage determinations (LCDs) for procedures and testing that include indications and restrictions along with approved diagnosis codes. Listed below are the four primary services that GI providers perform and provide interpretation for:

1. Evaluation and management (E&M) services: There are three criteria that have to be met to support any initial visit with patients: the history obtained, the examination performed, and the development of the treatment plan. There are five levels of service for office visits and three levels for inpatient visits, respectively. The levels are chosen based on the decision-making element of the visit, provided the documentation requirements are met for the level chosen. This is often not an easy selection unless the providers are educated on the E&M criteria. Auditors often see that visits are chosen by “guessing” the level, which leads to choosing either a lower or higher level of service than what was actually provided. Some providers have been instructed that E&M services are not that important since procedures are the major source of revenue for the practice. However, GI practices are visit-driven practices, and the initial visits are often worth more RVUs than some procedures. The E&M visit is truly vital and often the backbone for the medical necessity of any additional procedures and diagnostic services required in order for successful treatment of the patient.

2. Endoscopy and procedural billing: Here, medical necessity must be documented in order to submit charges for what was done. Gastroenterologists will often use multiple techniques when treating different areas within the gastrointestinal tract. Documentation has to include the location of lesions/abnormalities, method of treatment/removal, and the reason(s)/indication(s) for those procedures. There may be different instruments used in the colon (for example, snare in the sigmoid colon or biopsy forceps in the transverse colon). These may be separately reported with an appropriate modifier to indicate that these services were performed to different lesions/abnormalities. However, in order to bill for each of the procedures, all of this has to be documented in the endoscopy report. The physician is responsible for accurate and specific documentation and bringing charges back to the billing staff for claim submission. For a successful practice, a team approach is vital. Physicians and coding staff need to have an open line of communication to make sure that everything is submitted appropriately according to payer policies. Billing staff need to communicate any significant changes to the physicians/providers as these changes occur. Ignorance of payer policy is not considered an appropriate excuse when a payer investigates a claim and potential recoupment of moneys paid.

3. Diagnostic studies: Medical necessity/indication for the testing must be documented in order to submit charges for diagnostic studies. The terms “rule out” and “suspect” don’t completely give coders the reason why a physician suspects the patient might have a condition. Usually, abnormal lab tests, signs, and symptoms will often warrant the need for further investigation, and these are the most crucial indications for testing. Not only is this important for diagnostic studies but also for procedures. Make sure that the interpretation of the test results is clear along with a plan/recommendation(s).

4. Diagnosis codes: Assignment of codes per the International Classification of Diseases, 10th revision, Clinical Modification (ICD-10-CM) is the next and most important step after a visit, diagnostic study, and/or procedure. These codes support medical necessity for the services provided, and specificity of the diagnosis code is vital to successful submission and payment of a claim. Signs and symptoms are valid code choices when ruling out a more significant disease/diagnosis because these support medical necessity for a work-up to determine etiology. Comorbidities that impact the provider’s decision making should also be added as additional diagnoses to support the higher level of decision making. Up to 12 diagnosis codes can be assigned to any type of service provided. This also applies to preauthorization of all services, such as lab tests, radiology studies, GI diagnostic studies, and procedures. If specific information is not in the documentation for your staff to access, payers will often deny certain lab and radiology studies, as well as some procedures. There are 71,932 ICD-10-CM codes to choose from, and it is often difficult to find the “specific” code when doing a search in the electronic health record and billing system. Education and training are essential during the orientation sessions prior to active employment, as well as any time the system is upgraded. The providers should be willing to work with the IT representative(s) in the practice to help make the information easier to access. In other words, what “buzz” words would they like included in the description of the ICD-10-CM code in the practice’s list of favorites? For example, Crohn’s disease and ulcerative colitis have over a hundred choices. The choices are based on the location of the disease and whether the disease is without or with complications. If you are going to choose to provide a higher level of E&M service for a patient with Crohn’s disease of the large intestine because of exacerbation of the disease with bleeding, then the appropriate diagnosis code would be one of the following:

- K50.10 Crohn’s disease of large intestine without complications.

- K50.111 Crohn’s disease of large intestine with rectal bleeding.

- K50.112 Crohn’s disease of large intestine with intestinal obstruction.

- K50.113 Crohn’s disease of large intestine with fistula.

- K50.114 Crohn’s disease of large intestine with abscess.

- K50.118 Crohn’s disease of large intestine with other complication.

- K50.119 Crohn’s disease of large intestine with unspecified complications.

Getting paid for your provided services requires attention to detail and communication with your entire staffing team, including all providers. Make sure that your team is educated on all current issues and services pertaining to gastroenterology practices. If there is ever a question when reviewing a procedure note or any service, ask the provider who performed that service. Often, there will have to be legal corrections to the note before services can be billed. Making sure that the claim you are submitting is “clean” is essential for prompt payment. There are multiple resources available through the AGA that will help guide you with coding and billing. There are webinars, training sessions, and onsite services available via http://agau.gastro.org/diweb/catalog that can be provided for all providers, coding and billing staff, administrators, and clinical staff. Everyone needs to take an active role.

Ms. Mueller is a health care consultant with more than 35 years of experience in health care, including ICU/CCU nursing, physician office administration, GI claims submission and adjudication, and seminar instruction. She is president and owner of AskMueller Consulting in Lenzburg, Ill., which provides consulting services for physicians nationwide. Ms. Mueller is a nationally known speaker and the author of many multispecialty medical and surgical coding workbooks. She has a great amount of experience in gastroenterology, surgical subspecialties, and pediatric subspecialties. Her presentations have had audiences with the American Gastroenterological Association (AGA), North American Society for Pediatric Gastroenterology and Nutrition (NASPGAN), Society of Gastroenterology Nurses and Associates, Digestive Disease Week, American Pediatric Surgical Associations, and Decision Health and the Coding Institute. Ms. Mueller has written coding columns for ASGE, NASPGHAN, and AGA. She is the coeditor of the ASGE Coding Primer and also answers the coding hotline for the ASGE.

Planning for future college expenses with 529 accounts

Financial planning for families can involve multiple investment goals. The big ones usually are investing for retirement and for your children’s college expenses. With any investment strategy, once you have identified an investment goal, you will want to utilize the right investment account to achieve that goal. If investing for future college expenses is your goal, then one of the investment accounts you will want to utilize is called a 529 plan.

What is a 529 plan?

A 529 plan is a tax-favored account authorized by Section 529 of the Internal Revenue Code and sponsored by a state or educational institution. These plans have specific tax-saving features to them, compared with other taxable accounts, which are listed below. To begin with, there are two types of 529 plans: prepaid tuition plans and education savings plans. Every state has at least one type of 529 plan. Additionally, some private colleges sponsor a prepaid tuition plan.

Prepaid tuition plan

The first type of 529 account is a prepaid tuition plan. These let an account owner purchase college credits (or units) for participating colleges or universities at today’s prices to be used for the student’s future tuition charges. The states that sponsor prepaid plans do so primarily for the benefit of their in-state public colleges and universities. Things to know about the prepaid plans: States may or may not guarantee that the prepaid units keep up with increases in tuition charges. The plan also may have a state residency requirement. If the student decides not to attend one of the eligible schools, the equivalent payout may be less than had the student attended one of the participating institutions. There are no federal guarantees on the state prepaid plans and they are not available for private elementary and high school programs.

Education savings plan

The second type of 529 account is an education savings plan, an investment account into which you can invest your after-tax dollars. The intent with these accounts is to grow the balance for use at a future date. These are tax-deferred accounts, which means each year the interest, dividends, and capital gains created within the account do not show up on your tax return. If the funds are used for a “qualified” higher-education expense, then gains on the account are not taxed upon withdrawal.

As with most investments, the longer your money is invested, the more time it has to grow via accumulated interest, dividends, and appreciation. The larger the growth, the larger the tax benefits. This offers a tremendous advantage for a high-income and high-tax bracket household to invest for future goals (such as private school tuition or college expenses). By contrast, if you had invested in a fully taxable account, you would be subject to taxes each year on the interest, dividends, and capital gain distributions. Also, with taxable accounts, your investments would be subject to capital gains tax on the growth when they are sold to pay for those future expenses.

An account owner may choose among a range of investment options that the 529 plan provides. These are typically individual mutual funds or preformed mutual fund portfolios. The portfolios may have a fixed allocation percentage that stays the same over time or come “age-weighted,” meaning the investment allocation becomes more conservative the closer the student gets to college age when withdrawals would occur. This is a similar approach to the “target retirement date” offerings one sees in retirement accounts.

If one is using the 529 account for the student’s elementary or high school years, the investment time frame may be shorter and necessitate a more conservative approach, as the time for withdrawals would be nearer than the college years. As with most investments, the account can lose value based on investment performance.

Owner versus beneficiary

There are two parties to any 529 plan account: The account owner, who has control over the account and can name the beneficiary to the account, and the beneficiary (the student). The account owner can change beneficiaries on the account and can even name themselves as the beneficiary. One can name anyone as the beneficiary (e.g., child, friend, relative, yourself). You can be proactive by creating an account and naming yourself the beneficiary now, before switching to your child in the future. The account owner can live in one state with the beneficiary in another and invest in the 529 from a third state, and the student may eventually go to an educational institution in a fourth state. The 529 education savings account is not limited to any specific college, as a prepaid plan may be.

Withdrawals from 529s

If a 529 account withdrawal is for qualified higher education expenses or tuition for elementary or secondary schools, earnings are not subject to federal income tax or, in many cases, state income tax. Qualified withdrawals need to take place in the same tax year as the qualified expense.

Withdrawals not used for qualified higher education expenses in that year are considered “nonqualified” and would be subject to tax and 10% penalty on the earnings. State and local taxes may apply as well.

You can use the proceeds from the account free of taxes for the following qualified higher-education expenses:

- Tuition and school fees for both full and part time students at an eligible college, university, trade, or vocational institution.

- Room and board if the student is enrolled at more than half-time status. The amount up to the school’s room and board charges are eligible if paid directly to the school or to a landlord if living in nonschool housing. If actual charges to the landlord exceed the schools’ charges, then the amount above the school’s charges would be considered an excess withdrawal.

- Required books, supplies, and equipment for the academic program. Computer and technology equipment, printers, and required software, and such related services as Internet access also are qualified expenses.

- Private elementary or secondary school tuition up to $10,000 annually also is a qualified expense for 529 withdrawals.

Health insurance for the student and transportation-related costs to and from the school are not qualified expenses.

Contributions and fees

Like all investments, the fees associated with a 529 account need to be considered, as excess fees lower the investment returns. Prepaid tuition plans may charge initial application, transaction, and ongoing administrative fees. Investment 529 accounts may also have administrative costs such as program management fees, per-transaction fees, and the underlying investment expense ratios. Some states have broker-sold plans as well as direct-sold plans. Broker-sold plans can be purchased only through a broker and have the additional expenses associated with that either in the form of a load (sales charge) or higher expense ratio.

Contributions to a 529 plan can only be made in cash. If you currently have other investments, they need to be liquidated first (with the associated tax consequence) and then the proceeds invested into the 529 plan. Establishing the account and ongoing contributions are subject to gift tax limits ($15,000 for 2019). A married couple may make a “joint gift” to the account to double the limit. The 529 plans also allow the owner to front-load the account in 1 year with up to 5 years’ worth of gift limit contributions all at once. This lump sum is treated for tax reasons as a pro-rata 5 consecutive years of contributions all at once. Any additional gifts to that beneficiary during that year and the remaining four would be subject to gift tax issues if it means the annual gift limits were exceeded. Contributions are considered a “completed gift” for gift- and estate-tax purposes even though the account owner retains an element of control. The up-front 5-year gift election is available only on 529 accounts and is a great way for parents and grandparents (hint-hint) to reduce their estates and get a significant initial balance into the account. This can come in handy for those who may have procrastinated working toward this investment goal and need to catch up.

If the beneficiary does not need all or some of the funds for qualified higher education expenses, the account owner has options: One can change beneficiary to another relative who may need the funds or keep the account going and eventually add a grandchild as a beneficiary. Graduate school expenses also are eligible. A student can have multiple 529 accounts set up in their name.

Additional tax considerations

Education Tax Credits like the American Opportunity Tax Credit and the Lifetime Learning Credit have income phase-outs that you may or may not be eligible for based on your income. Education expenses used to qualify for the tax-free withdrawal from a 529 plan cannot be used to claim these tax credits. Several states offer state income tax deductions for contributions to a 529 plan but may have eligibility limited to the in-state plan only. It is wise to look to your own state’s plan first to see if that is the case and consider that as a factor when you choose a plan right for you. Refer to your tax professional for your eligibility.

In conclusion, 529 savings plans represent a tax-free way to grow your investments for future education expenses down the road, even if you don’t have a child yet. Speak to your financial adviser to learn about plans and contribution schedules that work with your current and future investing goals.

Good sources for further information include:

- www.savingforcollege.com.

- www.irs.gov/forms-pubs/about-publication-970.

- www.finra.org/investors/saving-college.

Mr. Clancy is director of financial planning, Drexel University College of Medicine.

Financial planning for families can involve multiple investment goals. The big ones usually are investing for retirement and for your children’s college expenses. With any investment strategy, once you have identified an investment goal, you will want to utilize the right investment account to achieve that goal. If investing for future college expenses is your goal, then one of the investment accounts you will want to utilize is called a 529 plan.

What is a 529 plan?

A 529 plan is a tax-favored account authorized by Section 529 of the Internal Revenue Code and sponsored by a state or educational institution. These plans have specific tax-saving features to them, compared with other taxable accounts, which are listed below. To begin with, there are two types of 529 plans: prepaid tuition plans and education savings plans. Every state has at least one type of 529 plan. Additionally, some private colleges sponsor a prepaid tuition plan.

Prepaid tuition plan

The first type of 529 account is a prepaid tuition plan. These let an account owner purchase college credits (or units) for participating colleges or universities at today’s prices to be used for the student’s future tuition charges. The states that sponsor prepaid plans do so primarily for the benefit of their in-state public colleges and universities. Things to know about the prepaid plans: States may or may not guarantee that the prepaid units keep up with increases in tuition charges. The plan also may have a state residency requirement. If the student decides not to attend one of the eligible schools, the equivalent payout may be less than had the student attended one of the participating institutions. There are no federal guarantees on the state prepaid plans and they are not available for private elementary and high school programs.

Education savings plan

The second type of 529 account is an education savings plan, an investment account into which you can invest your after-tax dollars. The intent with these accounts is to grow the balance for use at a future date. These are tax-deferred accounts, which means each year the interest, dividends, and capital gains created within the account do not show up on your tax return. If the funds are used for a “qualified” higher-education expense, then gains on the account are not taxed upon withdrawal.

As with most investments, the longer your money is invested, the more time it has to grow via accumulated interest, dividends, and appreciation. The larger the growth, the larger the tax benefits. This offers a tremendous advantage for a high-income and high-tax bracket household to invest for future goals (such as private school tuition or college expenses). By contrast, if you had invested in a fully taxable account, you would be subject to taxes each year on the interest, dividends, and capital gain distributions. Also, with taxable accounts, your investments would be subject to capital gains tax on the growth when they are sold to pay for those future expenses.

An account owner may choose among a range of investment options that the 529 plan provides. These are typically individual mutual funds or preformed mutual fund portfolios. The portfolios may have a fixed allocation percentage that stays the same over time or come “age-weighted,” meaning the investment allocation becomes more conservative the closer the student gets to college age when withdrawals would occur. This is a similar approach to the “target retirement date” offerings one sees in retirement accounts.

If one is using the 529 account for the student’s elementary or high school years, the investment time frame may be shorter and necessitate a more conservative approach, as the time for withdrawals would be nearer than the college years. As with most investments, the account can lose value based on investment performance.

Owner versus beneficiary

There are two parties to any 529 plan account: The account owner, who has control over the account and can name the beneficiary to the account, and the beneficiary (the student). The account owner can change beneficiaries on the account and can even name themselves as the beneficiary. One can name anyone as the beneficiary (e.g., child, friend, relative, yourself). You can be proactive by creating an account and naming yourself the beneficiary now, before switching to your child in the future. The account owner can live in one state with the beneficiary in another and invest in the 529 from a third state, and the student may eventually go to an educational institution in a fourth state. The 529 education savings account is not limited to any specific college, as a prepaid plan may be.

Withdrawals from 529s

If a 529 account withdrawal is for qualified higher education expenses or tuition for elementary or secondary schools, earnings are not subject to federal income tax or, in many cases, state income tax. Qualified withdrawals need to take place in the same tax year as the qualified expense.

Withdrawals not used for qualified higher education expenses in that year are considered “nonqualified” and would be subject to tax and 10% penalty on the earnings. State and local taxes may apply as well.

You can use the proceeds from the account free of taxes for the following qualified higher-education expenses:

- Tuition and school fees for both full and part time students at an eligible college, university, trade, or vocational institution.

- Room and board if the student is enrolled at more than half-time status. The amount up to the school’s room and board charges are eligible if paid directly to the school or to a landlord if living in nonschool housing. If actual charges to the landlord exceed the schools’ charges, then the amount above the school’s charges would be considered an excess withdrawal.

- Required books, supplies, and equipment for the academic program. Computer and technology equipment, printers, and required software, and such related services as Internet access also are qualified expenses.

- Private elementary or secondary school tuition up to $10,000 annually also is a qualified expense for 529 withdrawals.

Health insurance for the student and transportation-related costs to and from the school are not qualified expenses.

Contributions and fees

Like all investments, the fees associated with a 529 account need to be considered, as excess fees lower the investment returns. Prepaid tuition plans may charge initial application, transaction, and ongoing administrative fees. Investment 529 accounts may also have administrative costs such as program management fees, per-transaction fees, and the underlying investment expense ratios. Some states have broker-sold plans as well as direct-sold plans. Broker-sold plans can be purchased only through a broker and have the additional expenses associated with that either in the form of a load (sales charge) or higher expense ratio.

Contributions to a 529 plan can only be made in cash. If you currently have other investments, they need to be liquidated first (with the associated tax consequence) and then the proceeds invested into the 529 plan. Establishing the account and ongoing contributions are subject to gift tax limits ($15,000 for 2019). A married couple may make a “joint gift” to the account to double the limit. The 529 plans also allow the owner to front-load the account in 1 year with up to 5 years’ worth of gift limit contributions all at once. This lump sum is treated for tax reasons as a pro-rata 5 consecutive years of contributions all at once. Any additional gifts to that beneficiary during that year and the remaining four would be subject to gift tax issues if it means the annual gift limits were exceeded. Contributions are considered a “completed gift” for gift- and estate-tax purposes even though the account owner retains an element of control. The up-front 5-year gift election is available only on 529 accounts and is a great way for parents and grandparents (hint-hint) to reduce their estates and get a significant initial balance into the account. This can come in handy for those who may have procrastinated working toward this investment goal and need to catch up.

If the beneficiary does not need all or some of the funds for qualified higher education expenses, the account owner has options: One can change beneficiary to another relative who may need the funds or keep the account going and eventually add a grandchild as a beneficiary. Graduate school expenses also are eligible. A student can have multiple 529 accounts set up in their name.

Additional tax considerations

Education Tax Credits like the American Opportunity Tax Credit and the Lifetime Learning Credit have income phase-outs that you may or may not be eligible for based on your income. Education expenses used to qualify for the tax-free withdrawal from a 529 plan cannot be used to claim these tax credits. Several states offer state income tax deductions for contributions to a 529 plan but may have eligibility limited to the in-state plan only. It is wise to look to your own state’s plan first to see if that is the case and consider that as a factor when you choose a plan right for you. Refer to your tax professional for your eligibility.

In conclusion, 529 savings plans represent a tax-free way to grow your investments for future education expenses down the road, even if you don’t have a child yet. Speak to your financial adviser to learn about plans and contribution schedules that work with your current and future investing goals.

Good sources for further information include:

- www.savingforcollege.com.

- www.irs.gov/forms-pubs/about-publication-970.

- www.finra.org/investors/saving-college.

Mr. Clancy is director of financial planning, Drexel University College of Medicine.

Financial planning for families can involve multiple investment goals. The big ones usually are investing for retirement and for your children’s college expenses. With any investment strategy, once you have identified an investment goal, you will want to utilize the right investment account to achieve that goal. If investing for future college expenses is your goal, then one of the investment accounts you will want to utilize is called a 529 plan.

What is a 529 plan?

A 529 plan is a tax-favored account authorized by Section 529 of the Internal Revenue Code and sponsored by a state or educational institution. These plans have specific tax-saving features to them, compared with other taxable accounts, which are listed below. To begin with, there are two types of 529 plans: prepaid tuition plans and education savings plans. Every state has at least one type of 529 plan. Additionally, some private colleges sponsor a prepaid tuition plan.

Prepaid tuition plan

The first type of 529 account is a prepaid tuition plan. These let an account owner purchase college credits (or units) for participating colleges or universities at today’s prices to be used for the student’s future tuition charges. The states that sponsor prepaid plans do so primarily for the benefit of their in-state public colleges and universities. Things to know about the prepaid plans: States may or may not guarantee that the prepaid units keep up with increases in tuition charges. The plan also may have a state residency requirement. If the student decides not to attend one of the eligible schools, the equivalent payout may be less than had the student attended one of the participating institutions. There are no federal guarantees on the state prepaid plans and they are not available for private elementary and high school programs.

Education savings plan

The second type of 529 account is an education savings plan, an investment account into which you can invest your after-tax dollars. The intent with these accounts is to grow the balance for use at a future date. These are tax-deferred accounts, which means each year the interest, dividends, and capital gains created within the account do not show up on your tax return. If the funds are used for a “qualified” higher-education expense, then gains on the account are not taxed upon withdrawal.

As with most investments, the longer your money is invested, the more time it has to grow via accumulated interest, dividends, and appreciation. The larger the growth, the larger the tax benefits. This offers a tremendous advantage for a high-income and high-tax bracket household to invest for future goals (such as private school tuition or college expenses). By contrast, if you had invested in a fully taxable account, you would be subject to taxes each year on the interest, dividends, and capital gain distributions. Also, with taxable accounts, your investments would be subject to capital gains tax on the growth when they are sold to pay for those future expenses.

An account owner may choose among a range of investment options that the 529 plan provides. These are typically individual mutual funds or preformed mutual fund portfolios. The portfolios may have a fixed allocation percentage that stays the same over time or come “age-weighted,” meaning the investment allocation becomes more conservative the closer the student gets to college age when withdrawals would occur. This is a similar approach to the “target retirement date” offerings one sees in retirement accounts.

If one is using the 529 account for the student’s elementary or high school years, the investment time frame may be shorter and necessitate a more conservative approach, as the time for withdrawals would be nearer than the college years. As with most investments, the account can lose value based on investment performance.

Owner versus beneficiary

There are two parties to any 529 plan account: The account owner, who has control over the account and can name the beneficiary to the account, and the beneficiary (the student). The account owner can change beneficiaries on the account and can even name themselves as the beneficiary. One can name anyone as the beneficiary (e.g., child, friend, relative, yourself). You can be proactive by creating an account and naming yourself the beneficiary now, before switching to your child in the future. The account owner can live in one state with the beneficiary in another and invest in the 529 from a third state, and the student may eventually go to an educational institution in a fourth state. The 529 education savings account is not limited to any specific college, as a prepaid plan may be.

Withdrawals from 529s

If a 529 account withdrawal is for qualified higher education expenses or tuition for elementary or secondary schools, earnings are not subject to federal income tax or, in many cases, state income tax. Qualified withdrawals need to take place in the same tax year as the qualified expense.

Withdrawals not used for qualified higher education expenses in that year are considered “nonqualified” and would be subject to tax and 10% penalty on the earnings. State and local taxes may apply as well.

You can use the proceeds from the account free of taxes for the following qualified higher-education expenses:

- Tuition and school fees for both full and part time students at an eligible college, university, trade, or vocational institution.

- Room and board if the student is enrolled at more than half-time status. The amount up to the school’s room and board charges are eligible if paid directly to the school or to a landlord if living in nonschool housing. If actual charges to the landlord exceed the schools’ charges, then the amount above the school’s charges would be considered an excess withdrawal.

- Required books, supplies, and equipment for the academic program. Computer and technology equipment, printers, and required software, and such related services as Internet access also are qualified expenses.

- Private elementary or secondary school tuition up to $10,000 annually also is a qualified expense for 529 withdrawals.

Health insurance for the student and transportation-related costs to and from the school are not qualified expenses.

Contributions and fees

Like all investments, the fees associated with a 529 account need to be considered, as excess fees lower the investment returns. Prepaid tuition plans may charge initial application, transaction, and ongoing administrative fees. Investment 529 accounts may also have administrative costs such as program management fees, per-transaction fees, and the underlying investment expense ratios. Some states have broker-sold plans as well as direct-sold plans. Broker-sold plans can be purchased only through a broker and have the additional expenses associated with that either in the form of a load (sales charge) or higher expense ratio.

Contributions to a 529 plan can only be made in cash. If you currently have other investments, they need to be liquidated first (with the associated tax consequence) and then the proceeds invested into the 529 plan. Establishing the account and ongoing contributions are subject to gift tax limits ($15,000 for 2019). A married couple may make a “joint gift” to the account to double the limit. The 529 plans also allow the owner to front-load the account in 1 year with up to 5 years’ worth of gift limit contributions all at once. This lump sum is treated for tax reasons as a pro-rata 5 consecutive years of contributions all at once. Any additional gifts to that beneficiary during that year and the remaining four would be subject to gift tax issues if it means the annual gift limits were exceeded. Contributions are considered a “completed gift” for gift- and estate-tax purposes even though the account owner retains an element of control. The up-front 5-year gift election is available only on 529 accounts and is a great way for parents and grandparents (hint-hint) to reduce their estates and get a significant initial balance into the account. This can come in handy for those who may have procrastinated working toward this investment goal and need to catch up.

If the beneficiary does not need all or some of the funds for qualified higher education expenses, the account owner has options: One can change beneficiary to another relative who may need the funds or keep the account going and eventually add a grandchild as a beneficiary. Graduate school expenses also are eligible. A student can have multiple 529 accounts set up in their name.

Additional tax considerations

Education Tax Credits like the American Opportunity Tax Credit and the Lifetime Learning Credit have income phase-outs that you may or may not be eligible for based on your income. Education expenses used to qualify for the tax-free withdrawal from a 529 plan cannot be used to claim these tax credits. Several states offer state income tax deductions for contributions to a 529 plan but may have eligibility limited to the in-state plan only. It is wise to look to your own state’s plan first to see if that is the case and consider that as a factor when you choose a plan right for you. Refer to your tax professional for your eligibility.

In conclusion, 529 savings plans represent a tax-free way to grow your investments for future education expenses down the road, even if you don’t have a child yet. Speak to your financial adviser to learn about plans and contribution schedules that work with your current and future investing goals.

Good sources for further information include:

- www.savingforcollege.com.

- www.irs.gov/forms-pubs/about-publication-970.

- www.finra.org/investors/saving-college.

Mr. Clancy is director of financial planning, Drexel University College of Medicine.

Don’t let the mortgage preapproval process give you a stomachache

You are trying to buy your first home. Maybe you have heard stories from family, friends, and colleagues about nightmare scenarios when purchasing a home. There are many facets to the home-financing process, and a little bit of planning can reduce a significant amount of time and stress. Where do you begin? What do lenders look for when preapproving a borrower? What steps do I take to get preapproved for a mortgage loan? This article will help guide you through these initial stages to ultimately guide you to settlement on your new home.

Where to begin?

- Start by drafting a budget. How much of a monthly housing payment can you afford? Planning a budget is an extremely valuable exercise at any point in life, not just when buying a home. Often, borrowers will ask the question “How much can I afford?” The better question to ask is “Can I qualify for a home that meets the maximum monthly payment I have budgeted for?”

- What funds would I use for purchasing a home? Down payments and closing costs can add up quickly. Do you have funds readily available in an account you hold? Will you be obtaining a gift from a family member? Generally, funds for down payment are not allowed to be borrowed, unless the money is coming from an account secured by your own assets (for instance, borrowing from your own retirement account). Don’t think you necessarily need to put 20% down. Some loan programs offer little or no down payment options, while other programs may offer down payment assistance options.

- If you are not aware of your credit standing, run a free credit report to verify accurate information. Federal law allows consumers to access one free credit report annually with each of the three credit bureaus (Equifax, Experian, TransUnion). Knowing your credit history and data on your credit report is very important. If there are known or unknown issues on your credit report, it’s always best to at least be informed. You can access your free report at www.annualcreditreport.com.

- Start planning ahead with some of the documentation you will need for a loan approval. Lenders will request items such as tax returns and W-2s from the past 2 years, your recent pay stubs covering a 30-day period, most recent 2 months asset account statements (bank accounts, investment accounts, retirement accounts, etc.), as well as other documentation, depending on your specific scenario.

What are lenders looking at when preapproving an applicant?

Many people will often start to search for homes without having prepared for the preapproval process. This is not necessarily an issue and it doesn’t mean you will not be preapproved. Planning ahead could help you avoid any unforeseen problems and avoid rushing into the mortgage application process when trying to place an offer on a home.

In addition to supplying information on residence and employment/student history for the past 2 years, there are three primary components to a borrower’s credit portfolio:

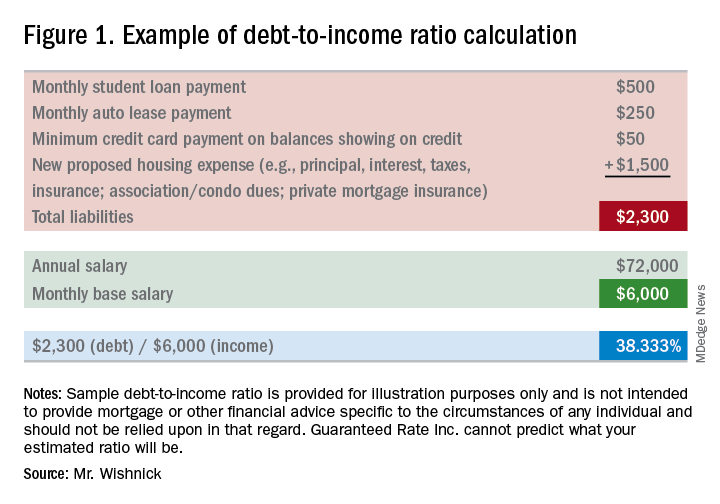

1) Debt-to-income ratio: What monthly expenses will show on your credit report (car loans/leases, student loans, credit card payments, personal loans/lines of credit, and mortgages for other properties owned)? Do you own any other real estate? Do you have other required obligations, such as alimony or child support payments? To calculate, first combine these liabilities on a monthly expense basis along with the new proposed monthly housing payment. Take these monthly liabilities and divide by monthly income. Gross income (pretax) for employees of a company they do not own is typically utilized (bonus or commission income can have some alternate rules to be allowed as qualifying income); for self-employed borrowers, tax returns will be required to be reviewed; tax write offs could reduce qualifying income. Self-employed individuals will typically need to show a 2-year income history via personal tax returns (as well as business tax returns if applicable). See Figure 1 for an example of a debt-to-income ratio calculation. Many loan programs will require a debt-to-income ratio of 45% or less. There are various loan programs that will be more or less restrictive than this percentage. A lender will be able to guide you to the proper program for your scenario.

2) Liquid assets: Lenders will review the amount of liquid funds you have available for down payment, closing costs, and any necessary reserves. These may include, but are not limited to, checking/savings/money market accounts, investment accounts (stocks, bonds, mutual funds), and retirement funds. Are there enough allowable funds available for the down payment and closing costs, as well as any required reserves needed for qualification? Large non–payroll deposits can be required to be sourced to make sure the funds are from an allowable source.

3) Credit history/scores: Buying a home will be one of the largest purchases you will make in a lifetime. Credit scores have a major impact on the cost of credit (the interest rate you will obtain). Having higher scores could result in a lower interest rate, as well as open up certain loan programs that may be more advantageous for you. Oftentimes, lenders will take the middle of the three scores as your mortgage score (one score from each of the three credit bureaus). In most cases, if applying jointly, the lowest of the middle scores for all borrowers is the score that is used as the score for the applicants. In general, a 740 middle credit score is considered to be excellent for mortgage financing but is not a requirement for all programs.

**You may have heard about specific mortgage programs for physicians. These programs are intended for use for lesser down payments, and/or not calculating student loan payments when qualifying for home financing. As future income potential is typically not considered when determining debt-to-income ratios, not counting these liabilities potentially increases borrowing power.

You are now ready to be preapproved for mortgage financing. What should you do next?

- Talk to a trusted lender. Ask your real estate agent, family, friends, or colleagues for local lender recommendations. Real estate agents will want to make sure you have spoken with a lender and completed a preapproval application to ensure that you can be preapproved for financing before showing you homes. If you need a loan to purchase a home, a preapproval letter will be required to submit with an offer letter. The application contains questions such as your address and employment history for the past 2 years, income and asset information, as well as a series of other financial information. A hard credit inquiry will need to be performed in order for the lender to issue a preapproval. What should you expect from a lender in addition to competitive rates and an array of programs? Some people prefer more of a hands-on approach. Working with a lender who provides regular status updates and makes him/herself easily accessible for all of your questions can certainly be an attractive feature. Working with a local lender also may be reassuring, as he or she should have plenty of experience with the market in which you are purchasing.

- Search for homes. Upon being given the green light for your preapproval and a price range within your comfort zone, connect with your local real estate professional to search for homes. Plan to spend time with your agent discussing all your needs for your new home.

- Submit an offer. Your lender will be able to provide an estimate of closing costs and monthly payments for homes that you are considering buying before you make an offer. You will want to be sure you are comfortable with the financial obligation prior to making your offer. With your offer, an initial good faith deposit (earnest money deposit) will be required. Your real estate agent will guide you on the proper amount of the deposit.

Conclusion

Once you and the seller have come to terms, you will look to discuss with your lender the rate and program options to secure (locking in an interest rate and program), as well as to complete the formal mortgage application. The lender will request additional documentation, if you have not already provided documents, in order for you to obtain a conditional mortgage commitment. The lender also will order an appraisal to ensure the property value supports the price you have agreed to pay for it. Your real estate agent will guide you through the various deadlines and requirements in the contract for items like home inspections, ordering a title search to obtain title insurance, and other nonfinancing contingencies. Some areas may require attorneys for contract review and closing, which your agent will discuss with you. As you can see, buying a home is not an instant process. Taking the appropriate steps to prepare for your mortgage preapproval could save you a lot of time and stress.

Mr. Wishnick is a 15-year mortgage industry veteran, vice president of mortgage lending with Guaranteed Rate (NMLS #2611) and was ranked as a Top 1% mortgage originator by Mortgage Executive Magazine. He can be reached at rob.wishnick@rate.com.

All information provided in this publication is for informational and educational purposes only, and in no way is any of the content contained herein to be construed as financial, investment, or legal advice or instruction. Guaranteed Rate does not guarantee the quality, accuracy, completeness or timelines of the information in this publication.

You are trying to buy your first home. Maybe you have heard stories from family, friends, and colleagues about nightmare scenarios when purchasing a home. There are many facets to the home-financing process, and a little bit of planning can reduce a significant amount of time and stress. Where do you begin? What do lenders look for when preapproving a borrower? What steps do I take to get preapproved for a mortgage loan? This article will help guide you through these initial stages to ultimately guide you to settlement on your new home.

Where to begin?

- Start by drafting a budget. How much of a monthly housing payment can you afford? Planning a budget is an extremely valuable exercise at any point in life, not just when buying a home. Often, borrowers will ask the question “How much can I afford?” The better question to ask is “Can I qualify for a home that meets the maximum monthly payment I have budgeted for?”

- What funds would I use for purchasing a home? Down payments and closing costs can add up quickly. Do you have funds readily available in an account you hold? Will you be obtaining a gift from a family member? Generally, funds for down payment are not allowed to be borrowed, unless the money is coming from an account secured by your own assets (for instance, borrowing from your own retirement account). Don’t think you necessarily need to put 20% down. Some loan programs offer little or no down payment options, while other programs may offer down payment assistance options.

- If you are not aware of your credit standing, run a free credit report to verify accurate information. Federal law allows consumers to access one free credit report annually with each of the three credit bureaus (Equifax, Experian, TransUnion). Knowing your credit history and data on your credit report is very important. If there are known or unknown issues on your credit report, it’s always best to at least be informed. You can access your free report at www.annualcreditreport.com.

- Start planning ahead with some of the documentation you will need for a loan approval. Lenders will request items such as tax returns and W-2s from the past 2 years, your recent pay stubs covering a 30-day period, most recent 2 months asset account statements (bank accounts, investment accounts, retirement accounts, etc.), as well as other documentation, depending on your specific scenario.

What are lenders looking at when preapproving an applicant?

Many people will often start to search for homes without having prepared for the preapproval process. This is not necessarily an issue and it doesn’t mean you will not be preapproved. Planning ahead could help you avoid any unforeseen problems and avoid rushing into the mortgage application process when trying to place an offer on a home.

In addition to supplying information on residence and employment/student history for the past 2 years, there are three primary components to a borrower’s credit portfolio:

1) Debt-to-income ratio: What monthly expenses will show on your credit report (car loans/leases, student loans, credit card payments, personal loans/lines of credit, and mortgages for other properties owned)? Do you own any other real estate? Do you have other required obligations, such as alimony or child support payments? To calculate, first combine these liabilities on a monthly expense basis along with the new proposed monthly housing payment. Take these monthly liabilities and divide by monthly income. Gross income (pretax) for employees of a company they do not own is typically utilized (bonus or commission income can have some alternate rules to be allowed as qualifying income); for self-employed borrowers, tax returns will be required to be reviewed; tax write offs could reduce qualifying income. Self-employed individuals will typically need to show a 2-year income history via personal tax returns (as well as business tax returns if applicable). See Figure 1 for an example of a debt-to-income ratio calculation. Many loan programs will require a debt-to-income ratio of 45% or less. There are various loan programs that will be more or less restrictive than this percentage. A lender will be able to guide you to the proper program for your scenario.

2) Liquid assets: Lenders will review the amount of liquid funds you have available for down payment, closing costs, and any necessary reserves. These may include, but are not limited to, checking/savings/money market accounts, investment accounts (stocks, bonds, mutual funds), and retirement funds. Are there enough allowable funds available for the down payment and closing costs, as well as any required reserves needed for qualification? Large non–payroll deposits can be required to be sourced to make sure the funds are from an allowable source.

3) Credit history/scores: Buying a home will be one of the largest purchases you will make in a lifetime. Credit scores have a major impact on the cost of credit (the interest rate you will obtain). Having higher scores could result in a lower interest rate, as well as open up certain loan programs that may be more advantageous for you. Oftentimes, lenders will take the middle of the three scores as your mortgage score (one score from each of the three credit bureaus). In most cases, if applying jointly, the lowest of the middle scores for all borrowers is the score that is used as the score for the applicants. In general, a 740 middle credit score is considered to be excellent for mortgage financing but is not a requirement for all programs.

**You may have heard about specific mortgage programs for physicians. These programs are intended for use for lesser down payments, and/or not calculating student loan payments when qualifying for home financing. As future income potential is typically not considered when determining debt-to-income ratios, not counting these liabilities potentially increases borrowing power.

You are now ready to be preapproved for mortgage financing. What should you do next?

- Talk to a trusted lender. Ask your real estate agent, family, friends, or colleagues for local lender recommendations. Real estate agents will want to make sure you have spoken with a lender and completed a preapproval application to ensure that you can be preapproved for financing before showing you homes. If you need a loan to purchase a home, a preapproval letter will be required to submit with an offer letter. The application contains questions such as your address and employment history for the past 2 years, income and asset information, as well as a series of other financial information. A hard credit inquiry will need to be performed in order for the lender to issue a preapproval. What should you expect from a lender in addition to competitive rates and an array of programs? Some people prefer more of a hands-on approach. Working with a lender who provides regular status updates and makes him/herself easily accessible for all of your questions can certainly be an attractive feature. Working with a local lender also may be reassuring, as he or she should have plenty of experience with the market in which you are purchasing.

- Search for homes. Upon being given the green light for your preapproval and a price range within your comfort zone, connect with your local real estate professional to search for homes. Plan to spend time with your agent discussing all your needs for your new home.

- Submit an offer. Your lender will be able to provide an estimate of closing costs and monthly payments for homes that you are considering buying before you make an offer. You will want to be sure you are comfortable with the financial obligation prior to making your offer. With your offer, an initial good faith deposit (earnest money deposit) will be required. Your real estate agent will guide you on the proper amount of the deposit.

Conclusion

Once you and the seller have come to terms, you will look to discuss with your lender the rate and program options to secure (locking in an interest rate and program), as well as to complete the formal mortgage application. The lender will request additional documentation, if you have not already provided documents, in order for you to obtain a conditional mortgage commitment. The lender also will order an appraisal to ensure the property value supports the price you have agreed to pay for it. Your real estate agent will guide you through the various deadlines and requirements in the contract for items like home inspections, ordering a title search to obtain title insurance, and other nonfinancing contingencies. Some areas may require attorneys for contract review and closing, which your agent will discuss with you. As you can see, buying a home is not an instant process. Taking the appropriate steps to prepare for your mortgage preapproval could save you a lot of time and stress.

Mr. Wishnick is a 15-year mortgage industry veteran, vice president of mortgage lending with Guaranteed Rate (NMLS #2611) and was ranked as a Top 1% mortgage originator by Mortgage Executive Magazine. He can be reached at rob.wishnick@rate.com.

All information provided in this publication is for informational and educational purposes only, and in no way is any of the content contained herein to be construed as financial, investment, or legal advice or instruction. Guaranteed Rate does not guarantee the quality, accuracy, completeness or timelines of the information in this publication.

You are trying to buy your first home. Maybe you have heard stories from family, friends, and colleagues about nightmare scenarios when purchasing a home. There are many facets to the home-financing process, and a little bit of planning can reduce a significant amount of time and stress. Where do you begin? What do lenders look for when preapproving a borrower? What steps do I take to get preapproved for a mortgage loan? This article will help guide you through these initial stages to ultimately guide you to settlement on your new home.

Where to begin?

- Start by drafting a budget. How much of a monthly housing payment can you afford? Planning a budget is an extremely valuable exercise at any point in life, not just when buying a home. Often, borrowers will ask the question “How much can I afford?” The better question to ask is “Can I qualify for a home that meets the maximum monthly payment I have budgeted for?”